A Beginners Guide to Estimated Quarterly Taxes

Every year millions of taxpayers pay quarterly estimated taxes. If you are unfamiliar with the process, it can seem daunting. The good news is that calculate and paying estimated taxes doesn’t have to be complicated. Read on to learn the basics of who, how, where and when to make the estimated payments.

Who Has to Make Estimated Tax Payments?

Chances are if you owed over $1,000 on your last income tax return, you have to make estimated tax payments. Even if you didn’t owe last year, but expect to owe this year, you should calculate and make the payments to avoid penalties.

The most common reasons people need to make estimated payments are because they have:

· Self-employment income

· Dividend or interest income over $600

· Rental income

· Side-hustle or freelance income

For employees, most of their taxes are paid through paycheck deductions. It’s unlikely they will need to make estimated payments unless they make any income listed above. If you are an employee and owed taxes when you last filed, then you may want to check your payroll paperwork, specifically your W-4, on file with your employer.

How to Calculate Quarterly Tax Payments

There are two main ways to calculate how much to pay for quarterly taxes. First, we will go through the harder option before covering the simple method.

The first way to calculate the estimated tax payment is by basically preparing a mini tax return. Using the IRS form 1040-ES, enter in all your estimated income, deductions, and credits. You will enter the amounts for the entire year. You can even calculate any self-employment taxes on the same form.

By following the form, you’ll arrive at your estimated annual taxes due and divide it into quarterly estimated tax payments. Be sure to read the instructions carefully and talk to a professional if you need help. You need to pay at least 90% of the years taxes via estimated payments to avoid penalties.

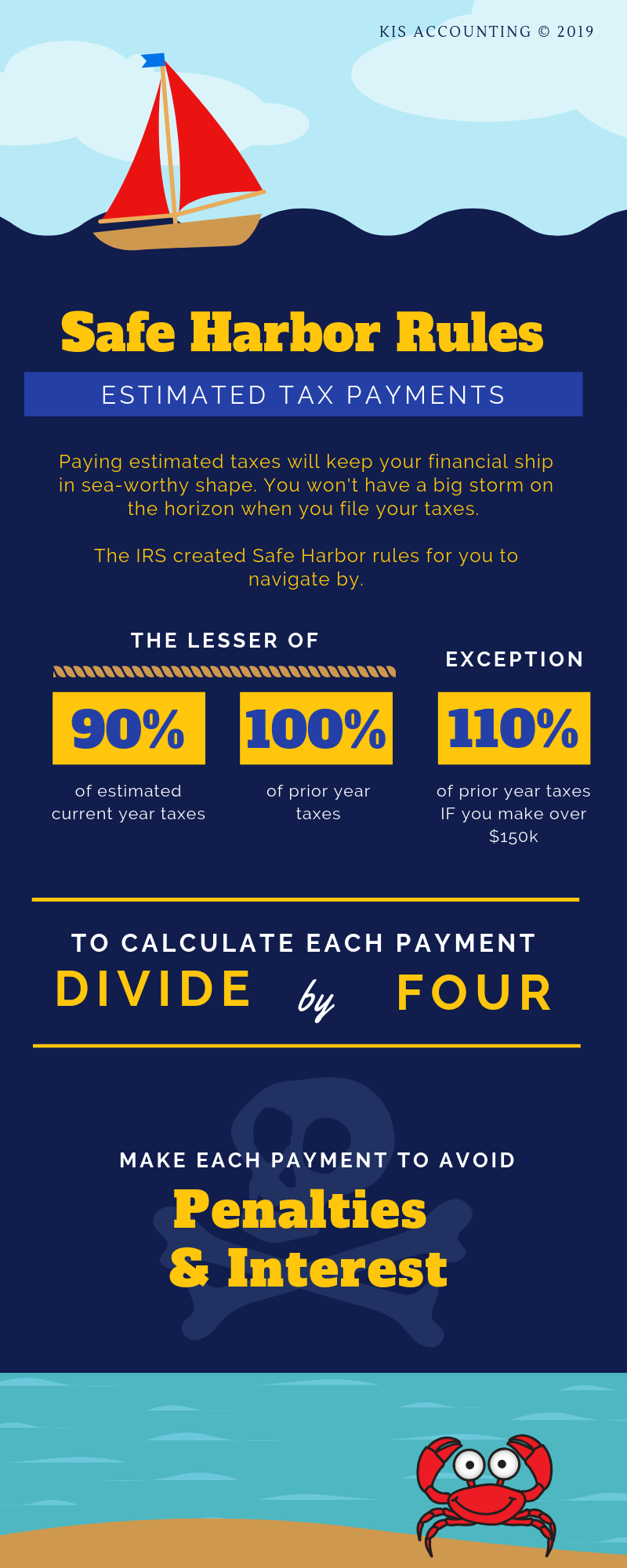

The second way to calculate your quarterly tax payments is much simpler! Essentially, you pay taxes based off your prior year return. These are what the IRS calls “Safe Harbor Rules.”

There are three ways to stay in the safe harbor.

Pay 100% of your prior year tax liability.

Pay 90% of your current year tax liability (you’ll need to estimate your annual taxes using the 1040-ES and possibly adjust the payment amounts if your estimates prove far different from your actual income and tax calculation).

If you earn over $150,000, pay 110% of your prior year liability.

Any tax preparer can give you vouchers for 100% or 110% of your prior year tax liability when you file that year’s tax return. Make sure to ask them for the vouchers!

To help you remember these guidelines, we created this nautical infographic.

{kind=link}

Where/How to Pay Quarterly Taxes

Individuals can pay estimated taxes a variety of ways. The most common are to pay them online at irs.gov/payments or to send a check in the mail along with the estimated tax voucher.

Other options to pay include over the phone, cash at registered partners, or even through their mobile app.

When are the Due Dates?

Estimated taxes are due near the end of each quarter. Below are the due dates for 2019 estimated tax payments:

1st Quarter: April 15, 2019

2nd Quarter: June 17, 2019

3rd Quarter: Sept. 16, 2019

4th Quarter: Jan. 15, 2020

Most payments are due on the 15th of the respective month, unless it’s a holiday or weekend. Then it’s due on the following business day.

A Note on State Taxes

If you pay income taxes to your state and have to pay estimated taxes to the IRS, then it’s likely you’ll have to pay estimated taxes to your state as well. Every state is different so you will need to follow your state’s guidance. In general, the calculations are based off your federal return so most of the hard work is done.

With this information, you are well on your way to paying your estimated taxes accurately and on time. If you get stuck in the process, send us a note and we’ll be glad to help you out.

If you owe estimated taxes, it’s important to make them. For most people, it’s easier to make four smaller payments over a year than one large payment at one time. You’ll save money by avoiding penalties and interest and give yourself peace of mind knowing you are in good standing with the IRS.